Recording mistakes are common. Research from EY summarized by HR Dive found that employers average 15 payroll corrections per pay period, with cafeteria plan deduction errors among the costliest categories. Many of those errors trace back to deductions configured with the wrong tax treatment, amounts that don't match carrier invoices, or enrollment changes that never made it into payroll.

This guide covers the foundational setup you need before recording, a step-by-step process for journal entries and remittance, the key variables that change how entries work, and the mistakes that derail payroll teams most often.

TL;DR

- Health insurance deductions create two separate recording obligations: the employee's withheld share (a liability) and the employer's contribution (an expense)

- Pre-tax deductions under a Section 125 cafeteria plan reduce taxable wages before FICA and federal income tax are calculated — post-tax deductions do not

- The full lifecycle runs: enrollment → payroll setup → per-period journal entries → carrier remittance → W-2 reporting

- Most errors come from wrong tax-treatment configuration, stale enrollment data, or skipping the carrier invoice reconciliation step

- Accurate recording requires three prerequisites: clean enrollment data, a structured chart of accounts, and correct deduction code setup

What You Need Before Recording Health Insurance Deductions

Errors don't start at the journal entry — they start upstream. Three inputs must be in place before processing begins.

Plan and Enrollment Data

You need four specific data points per employee:

- Total monthly premium for their elected plan

- Employer-employee cost split (e.g., employer covers 80%, employee covers 20%)

- Coverage tier — employee-only, employee + spouse, or family (each tier has a different premium)

- Coverage effective date — determines when deductions start and stop

These amounts vary by employee. A team where some employees carry family coverage and others have single plans cannot use one flat deduction rate across everyone.

For HR Tech and benefits platforms managing enrollment across multiple systems, Bindbee's Benefits Enrollment Sync surfaces plan selections, coverage tiers, contribution amounts, and effective dates as normalized fields. It also writes deduction data back to connected payroll systems in real time, eliminating the manual step of translating enrollment elections into payroll deduction amounts.

Chart of Accounts Setup

Before posting any entries, confirm these three accounts exist in your chart of accounts:

| Account | Type | Purpose |

|---|---|---|

| Employee Health Insurance Withholdings Payable | Current Liability | Holds employee-withheld amounts until remitted |

| Health Insurance Expense | Expense | Records employer's cost contribution |

| Health Insurance Payable (Employer) | Current Liability | Accrues employer's share until carrier is paid |

Using the wrong account type — for example, booking the employee withholding directly to expense — misstates both the balance sheet and income statement.

Deduction Tax Treatment Confirmation

Verify whether your plan qualifies as a Section 125 cafeteria plan before configuring anything. This single determination affects:

- Whether Social Security, Medicare, and federal income taxes are calculated on gross pay or reduced pay

- How the deduction code is flagged in your payroll system

- What appears in W-2 Boxes 1, 3, and 5

If you're unsure, check whether the company has a written Section 125 plan document on file. No document means no pre-tax treatment, regardless of how the deduction code is configured.

How to Record Employee Health Insurance Deductions in Payroll

Recording spans five distinct steps: system setup, per-period journal entries, carrier remittance, reconciliation, and year-end W-2 confirmation.

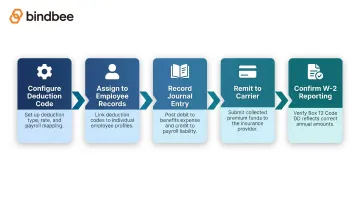

Step 1: Configure the Deduction Code

In your payroll system, create a deduction code specifically for health insurance. The configuration determines everything downstream.

For a Section 125 pre-tax plan:

- Flag the deduction to exclude from federal income tax, Social Security, and Medicare wage bases

- Taxes must be calculated after the deduction is applied, not before

- Map the deduction to the Employee Health Insurance Withholdings Payable liability account

For the employer contribution:

- Create a separate employer benefit code

- Map it to the Health Insurance Expense account

- Set the calculation method — fixed dollar amount per pay period is standard

Step 2: Assign Deductions to Employee Records

Enter each employee's specific per-period withholding amount based on their coverage tier. Then confirm:

- Deduction frequency matches the pay cycle (biweekly = 26 periods/year; semi-monthly = 24)

- Per-period amount is calculated by dividing the annual employee premium share by the correct number of pay periods

- Each employee's record reflects their actual elected tier, not a company-wide average

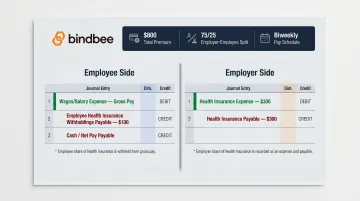

Step 3: Record the Journal Entry at Each Pay Run

Employee deduction side:

| Account | Debit | Credit |

|---|---|---|

| Wages/Salaries Expense (gross pay) | $X | |

| Employee Health Insurance Withholdings Payable | $100 | |

| Cash/Payroll Clearing (net pay + other withholdings) | $X - $100 |

Employer contribution side (recorded simultaneously):

| Account | Debit | Credit |

|---|---|---|

| Health Insurance Expense | $100 | |

| Health Insurance Payable | $100 |

Worked example: Total monthly premium is $800. The employer pays 75% ($600/month), the employee pays 25% ($200/month). On a biweekly schedule, the employee's per-period deduction is $200 ÷ 2 = $100, and the employer's per-period accrual is $600 ÷ 2 = $300. Both sides post simultaneously at each payroll run.

Step 4: Remit to the Carrier and Clear the Liability

When the carrier invoice is paid, clear both payable accounts:

| Account | Debit | Credit |

|---|---|---|

| Employee Health Insurance Withholdings Payable | $X | |

| Health Insurance Payable | $X | |

| Cash/Bank | $X + $X |

At this point, reconcile the payment against the carrier invoice and your total withheld amounts.

Any gap between what was withheld and what the invoice shows typically signals an enrollment change (a new dependent, a tier upgrade, or a termination) that wasn't reflected in payroll.

Step 5: Confirm W-2 Reporting at Year-End

Two things must be true on every employee's W-2:

Box 12, Code DD — the total cost of coverage (employer + employee premiums combined) is reported here. Per IRS W-2 reporting guidance, this is informational only and does not increase taxable wages.

Boxes 1, 3, and 5 — pre-tax Section 125 employee premiums must be excluded from all three boxes, reducing reported federal taxable wages, Social Security wages, and Medicare wages.

Run a W-2 dry run before filing season. Catching a misconfigured pre-tax deduction in November is far less disruptive than filing W-2cs in March.

Key Variables That Affect How Deductions Are Recorded

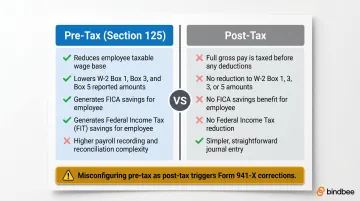

Pre-Tax vs. Post-Tax Treatment

This is the single most consequential configuration decision.

| Factor | Pre-Tax (Section 125) | Post-Tax |

|---|---|---|

| Taxable wage base | Reduced before FICA and FIT | Full gross pay taxed first |

| W-2 Boxes 1, 3, 5 | Reduced by deduction amount | No reduction |

| Employee tax savings | Yes — FICA + FIT on lower wages | None |

| Recording complexity | Higher — requires correct wage-base calculation | Simpler entry |

Misconfiguring a pre-tax plan as post-tax means employees overpay FICA all year. Correcting it retroactively requires Form 941-X for each affected quarter and W-2c for each employee.

Employer vs. Employee Contribution Split

KFF's 2025 Employer Health Benefits Survey reports that employers cover an average of 84% of single coverage premiums ($7,885 of the $9,325 average annual premium). That majority-employer split means the employer side of the entry is typically larger than the employee side.

Recording discipline matters here: the employee's withheld share flows through a liability account (money you're holding on their behalf), while the employer's share is a direct expense. Booking both to expense overstates operating costs during the pay period and creates a reconciliation problem when the carrier is paid.

Pay Frequency and Per-Period Amounts

The same annual premium produces different per-period deductions depending on schedule:

- Biweekly (26 periods): divide the annual employee share by 26 — a $1,200 premium becomes $46.15/period

- Semi-monthly (24 periods): divide by 24 — the same $1,200 premium becomes $50.00/period

Use the wrong divisor and you'll either under-withhold or over-withhold all year — and the carrier invoice won't match.

Mid-Period Enrollment Changes

New hires enrolling mid-pay-period, employees adding dependents after a qualifying life event, and terminations all require deduction updates. Payroll systems that depend on manual data entry from HR or benefits teams are the most vulnerable here.

Automated infrastructure closes this gap by pushing changes in real time rather than waiting for a manual file transfer or the next scheduled payroll run. Bindbee's webhook infrastructure, for example, fires events for qualifying life events (terminations, dependent additions, coverage tier changes), sending structured data to connected payroll systems the moment the change occurs in the HRIS.

Common Mistakes When Recording Health Insurance Deductions

Most recording errors are configuration or process failures, not knowledge gaps. They're also easy to miss until W-2 season or an audit.

Misclassifying a pre-tax plan as post-tax. Employees overpay FICA throughout the year. Fixing it mid-year means filing Form 941-X for each affected quarter and issuing corrected W-2c forms — entirely avoidable if the plan type is verified at setup.

Booking the employee's withheld amount to expense. The withheld amount is not your cost — it's money you're holding temporarily on the employee's behalf. It belongs in a liability account. Expensing it inflates costs during the pay period and leaves a hanging balance when you remit to the carrier.

Skipping period-end reconciliation against the carrier invoice. Plan premiums change with open enrollment cycles, dependent additions, and coverage tier changes. If payroll is running last year's deduction amounts against a new plan year's invoices, the liability account will never clear correctly.

Leaving enrollment changes out of payroll. Manual processes for communicating benefits changes from an HRIS or benefits platform to payroll are a reliable source of stale deduction amounts. HR Executive notes that mapping issues during open enrollment frequently trigger incorrect deductions that go undetected until after the fact. Automated enrollment-to-payroll sync closes this gap: deduction amounts update when an employee changes coverage tiers, with no manual handoff required.

Frequently Asked Questions

How do you record employee benefits in accounting?

Employee benefits are recorded through a combination of expense accounts (for the employer-paid portion) and liability accounts (for amounts withheld from employees pending payment to the provider). The specific accounts depend on the benefit type and whether contributions are pre-tax or post-tax under a Section 125 plan.

How do you record the employee portion of health insurance?

The employee's withheld share is credited to a current liability account — typically "Employee Health Insurance Withholdings Payable" — at the time of payroll. That liability is cleared when the employer remits payment to the insurance carrier.

What is the difference between pre-tax and post-tax health insurance deductions?

Pre-tax deductions under a Section 125 cafeteria plan are subtracted from gross pay before federal income tax, Social Security, and Medicare are calculated, reducing the employee's taxable wages. Post-tax deductions come out after taxes, so the employee's full gross pay is taxed first and there's no FICA savings.

How does the employer contribution to health insurance get recorded?

The employer's share of the premium is debited to a Health Insurance Expense account and credited to a Health Insurance Payable liability account at payroll posting. When the carrier invoice is paid, the payable is debited and cash is credited.

What accounts are used to record health insurance deductions?

Three core accounts handle these entries:

- Employee Health Insurance Withholdings Payable — current liability for the withheld employee portion

- Health Insurance Payable — accrued liability for the employer's contribution (both cleared at carrier remittance)

- Health Insurance Expense — records the employer's cost share

How do health insurance deductions appear on a W-2?

The total cost of employer-sponsored health coverage — employer and employee premiums combined — is reported in Box 12 with Code DD for informational purposes only. Pre-tax employee premiums are excluded from Boxes 1, 3, and 5, reducing reported taxable and FICA wages accordingly.