The result: dropped transactions, failed checkouts, and compliance exposure across health apps, telehealth platforms, and digital pharmacies.

Picking the wrong API — or defaulting to a general-purpose processor without proper configuration — creates systematic declines that erode user trust and leave revenue on the table. This guide covers the top APIs built or configured for HSA/FSA compliance, what separates them technically, and how to evaluate them for your platform.

TL;DR

- HSA/FSA cards operate under IRS Section 213(d) rules and card-network restrictions that standard payment APIs don't enforce by default

- Core compliance requirements: IRS-qualified expense validation, IIAS support, healthcare MCC codes, PCI DSS v4.0.1 compliance, and split-tender handling

- Top APIs for HSA/FSA payments: Flex, Stripe (with configuration), Adyen, Truemed, and NMI — each suited to different platform types

- Choose based on regulatory fit, real-time eligibility enforcement, and how well the API connects to your benefits enrollment data

Why HSA/FSA Payment APIs Are Different from Standard Gateways

HSA and FSA cards are tax-advantaged spending instruments governed by IRS Section 213(d) — not standard debit cards. The payment system itself is responsible for enforcing eligibility at the point of authorization, and most engineering teams don't realize this until their first declined transaction.

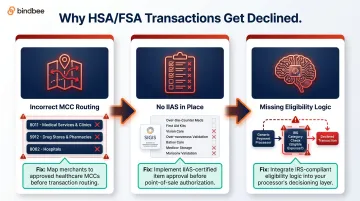

Three Reasons Legitimate Transactions Get Declined

Incorrect MCC routing: Visa and Mastercard restrict HSA/FSA cards to approved healthcare Merchant Category Codes (8011 for physicians, 5912 for pharmacies, 8062 for hospitals). Transactions routed through any other MCC are automatically declined, regardless of whether the item qualifies medically.

No IIAS in place: Merchants outside a qualifying healthcare MCC must implement an Inventory Information Approval System (IIAS), governed by SIGIS, that validates item-level eligibility at checkout. Without it, FSA card networks won't authorize the transaction.

Missing eligibility logic: Generic processors treat HSA/FSA cards as standard debit. They don't validate IRS categories, don't flag mixed carts, and route everything identically. When the card network checks, it fails.

The 90% Rule Exception

Drug stores and pharmacies where 90%+ of gross sales are eligible medical items can bypass IIAS entirely and process HSA/FSA cards like any other payment card. Annual re-attestation with SIGIS is required, though. Most digital health platforms won't meet this threshold.

What a Proper HSA/FSA API Must Handle

| Requirement | Why It Matters |

|---|---|

| IRS Section 213(d) enforcement | Validates that purchases qualify as medical expenses |

| IIAS integration or native eligibility | Enables item-level approval at checkout |

| Healthcare MCC configuration | Ensures card network routing succeeds |

| Split-tender logic | Handles mixed carts (eligible + ineligible items) |

| Audit-ready transaction logging | Supports compliance reviews and dispute resolution |

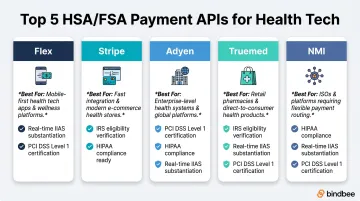

Best APIs for HSA & FSA Payments in Health Tech

These five APIs cover the full range of HSA/FSA use cases in health tech — from in-app subscriptions and DTC retail to enterprise pharmacy and ISO platforms. Each was evaluated on compliance architecture, developer integration quality, HSA/FSA-specific feature support, and real-world deployment.

Flex

Flex is a purpose-built HSA/FSA payment infrastructure layer designed specifically for digital health and wellness apps. It handles IRS and plan compliance on the developer's behalf — eligibility validation, LMN workflows, mixed cart handling — so engineering teams don't have to build that logic themselves.

The standout capability: its November 2025 RevenueCat integration enables HSA/FSA payments for in-app subscriptions on iOS, Android, and web apps. This was previously impossible due to Apple's in-app purchase requirements. By working within Apple's external billing allowance, Flex opened a revenue channel that no general-purpose processor covers.

A real-world example: Ladder, the strength training app with 100,000+ App Store reviews, partnered with Flex to accept HSA/FSA for memberships — with members saving 30–40% via pre-tax dollars.

| Category | Detail |

|---|---|

| Best For | Digital health apps and wellness subscription platforms requiring in-app HSA/FSA acceptance |

| Key Compliance Features | Native IRS and plan rule enforcement, built-in eligibility validation, LMN workflow, mixed cart support |

| Developer Integration | Clean API at docs.withflex.com, documented RevenueCat integration, minimal engineering lift |

Stripe

For most health tech teams, Stripe is already in the stack. It does support HSA/FSA card acceptance — but not by default. Teams must correctly configure their merchant Industry setting in Stripe's dashboard, and that misconfiguration is one of the most commonly cited causes of FSA/HSA payment failures in production.

Stripe offers three paths to HSA/FSA acceptance: qualifying healthcare MCC, 90% attestation, or IIAS certification integration. None of these are automatic. Stripe also does not provide a native eligibility verification layer, LMN workflow, or SIGIS product eligibility list — each must be sourced and configured separately.

Where Stripe earns its place: PCI DSS Level 1 certification, best-in-class webhook infrastructure, tokenization, subscription billing, and a developer ecosystem that's hard to match. For teams already running on Stripe, adding HSA/FSA support is achievable — it just requires additional configuration and potentially a third-party eligibility layer.

| Category | Detail |

|---|---|

| Best For | Telehealth platforms and health SaaS with existing Stripe infrastructure |

| Key Compliance Features | PCI DSS L1, tokenization, webhooks — HSA/FSA eligibility requires additional configuration |

| Developer Integration | Extensive SDK and API documentation, sandbox environment, strong developer community |

Adyen

Adyen is an enterprise-grade payment platform with direct acquiring capabilities across multiple markets. For large health tech companies, its ability to configure custom MCCs and route transactions through direct network connections (without an intermediary acquirer) gives it a meaningful edge in accuracy and latency.

Adyen's healthcare portfolio is documented: Rectangle Health, serving thousands of healthcare providers for over 30 years, uses Adyen's embedded platform to automate insurance reimbursements and manage patient payment revenue cycles.

The platform's fraud prevention and compliance infrastructure also aligns well with HIPAA-aligned security requirements, though teams should independently evaluate specific HIPAA obligations for their data flows.

| Category | Detail |

|---|---|

| Best For | Enterprise health tech platforms and digital pharmacies scaling across multiple markets |

| Key Compliance Features | Custom MCC configuration, advanced fraud prevention, PCI DSS Level 1, direct acquiring |

| Developer Integration | Robust API documentation at docs.adyen.com, SDKs, dedicated implementation support for enterprise customers |

Truemed

Truemed operates at the merchant layer rather than the MCC or IIAS layer. Its clinical intake and Letter of Medical Necessity (LMN) workflow connects patients with licensed practitioners to qualify purchases that wouldn't otherwise be HSA-eligible — a critical distinction for wellness brands outside traditional healthcare MCCs.

This makes Truemed particularly relevant for DTC health retailers and wellness brands selling fitness equipment, supplements, or other products that wouldn't qualify under a standard healthcare MCC. The platform is trusted by 3,000+ health brands including Garmin, Peloton, Eight Sleep, and AG1.

The conversion data is compelling: Shopify merchants using Truemed see 22% higher average order values and 10% higher conversion rates. The Shopify integration requires no custom code and can go live in 15 minutes.

| Category | Detail |

|---|---|

| Best For | DTC health retailers and wellness brands selling products that need eligibility qualification |

| Key Compliance Features | LMN-based eligibility qualification, HIPAA-compliant intake, SOC 2 Type II, IRS-aligned documentation |

| Developer Integration | Native Shopify app, partner support portal at support.truemed.com, integrates with major e-commerce platforms |

NMI (Network Merchants Inc.)

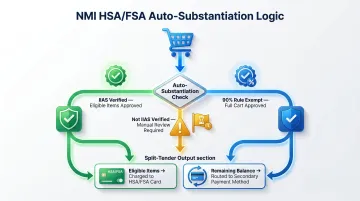

NMI is the strongest option for merchants operating across both physical and online channels. Its gateway comes with native IIAS support and auto-substantiation built in, covering card-present and card-not-present transactions where MCC handling and IIAS validation must work in both environments.

NMI supports three substantiation modes per transaction: verified against IIAS, not verified against IIAS, and exempt by the 90% Rule. Its auto-substantiation logic identifies eligible items in the cart, initiates a transaction for only those items, and routes the remaining balance to a separate payment method, handling split-tender natively.

NMI's FSA/HSA processing is available for merchants on the TSYS platform, processing via Visa and Mastercard, with a defined list of qualifying healthcare MCCs.

| Category | Detail |

|---|---|

| Best For | ISOs, SaaS platforms, and health retailers needing IIAS support and mixed-MCC handling |

| Key Compliance Features | IIAS integration, enhanced MCC logic, auto-substantiation, card-present and card-not-present support |

| Developer Integration | Developer portal at docs.nmi.com, sandbox environment, SDK and API access |

Key Features to Look for in an HSA/FSA Payment API

IRS Eligibility Enforcement and IIAS Compatibility

The API must validate — or support validation of — qualified medical expenses under IRS Section 213(d). Without IIAS or a healthcare MCC, eligible transactions get declined and non-eligible transactions may be incorrectly approved. Both create compliance and tax exposure.

The two compliant paths:

- Healthcare MCC — assigned by the card network, enables direct HSA/FSA acceptance without SIGIS registration

- IIAS certification — required for merchants with non-healthcare MCCs, enables item-level eligibility filtering at checkout

Healthcare MCC Configuration and Split-Tender Logic

Incorrect MCC setup is one of the most common causes of unnecessary declines — and it's entirely preventable. The platform must also handle split-tender payments for mixed carts, routing eligible items to the HSA/FSA card and the remaining balance to a secondary payment method. This is non-negotiable for any health retailer or wellness platform selling a combination of eligible and ineligible products.

PCI DSS Compliance, Tokenization, and Audit Logging

As of March 31, 2025, PCI DSS v4.0.1 is the only active standard. Any payment API being evaluated today must be validated against v4.0.1, not the retired v3.2.1. Required elements:

- PCI DSS Level 1 service provider certification

- Tokenized card storage to reduce compliance scope and protect health payment data

- Audit-ready logging that records eligibility checks, authorization outcomes, and IRS validation events

Subscription Billing and Telehealth Payment Support

Health apps and telehealth platforms need recurring HSA/FSA card charges to work reliably. Core requirements include:

- Smart retry logic to handle authorization failures without disrupting service

- Subscription renewal handling that re-validates eligibility at each billing cycle

- Webhook-based service activation tied to successful charge events

Flex's RevenueCat integration and Truemed's recurring order support address this at the infrastructure level. Stripe can handle recurring HSA/FSA charges with proper configuration, but eligibility substantiation per charge must be managed separately.

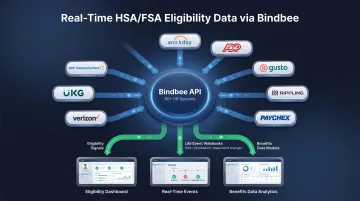

Upstream Benefits Eligibility Data Integration

Most payment API evaluations skip this layer entirely. Payment accuracy depends on knowing — before the transaction is attempted — whether an employee is enrolled in an HSA or FSA, what their contribution limits are, and whether a qualifying life event has changed their status.

Platforms that pull real-time enrollment data from HRIS and payroll systems can catch stale records before they cause authorization failures. Bindbee connects to 60+ HR systems and delivers:

- Real-time eligibility signals across Workday, ADP, Gusto, Rippling, Paychex, UKG, and SAP SuccessFactors

- Webhook notifications for life events — new hires, terminations, and dependent changes

- Structured data models for employee benefits, dependent benefits, and employer benefits

ThrivePass cut their HSA/FSA audit cycles from six weeks to under one week by streaming real-time eligibility through Bindbee rather than relying on manual payroll exports.

How We Chose These APIs

Each API was assessed on four criteria:

- Native or configurable HSA/FSA compliance: IRS eligibility enforcement, IIAS support, MCC handling, split-tender logic

- Developer integration quality: documentation depth, sandbox environment, SDK availability, webhook support

- Real-world health tech fit: whether the API is designed for or demonstrably used in telehealth, digital health apps, health retail, or benefits tech

- Integration speed: how quickly a team can move from sandbox to production with compliant HSA/FSA transaction processing

Security and compliance certifications were weighted heavily, specifically PCI DSS Level 1 and HIPAA-readiness for any API handling protected health information. Health payment data carries both financial and medical privacy requirements, and the two don't always get evaluated together.

Health tech engineering teams are typically under compliance timelines with limited bandwidth — which is precisely why integration speed made it onto the criteria list alongside compliance depth.

One mistake worth naming directly: selecting a general-purpose payment gateway and assuming it handles HSA/FSA compliance out of the box. Stripe is powerful, but enabling it without MCC setup or an eligibility layer produces systematic declines. The same holds for any processor not purpose-built for healthcare transactions.

Conclusion

HSA and FSA payment processing demands more than API selection. You need the right compliance architecture — correct MCC, IIAS or LMN-based eligibility, split-tender support, PCI DSS v4.0.1 compliance — and accurate, real-time enrollment data to ensure transactions are approved for the right people and the right expenses.

Defaulting to a familiar processor without proper configuration is one of the most expensive mistakes health tech teams make, and it's avoidable.

Before evaluating payment APIs, evaluate your data layer. Does your platform have access to real-time HSA/FSA enrollment status, contribution data, and life event triggers from your customers' employer systems? If not, your authorization rates will reflect that gap regardless of which payment API you choose.

That data gap is where Bindbee operates. It connects benefits and HRIS data across 60+ systems through a single API, giving health tech platforms the real-time eligibility signals needed to reduce authorization errors upstream of payment.

The results are concrete: Healthee cut integration deployment time from 8–12 weeks to 24–48 hours; ThrivePass reduced HSA/FSA audit cycles from six weeks to under one week.

If your platform handles HSA/FSA payments, start by auditing your enrollment data pipeline — because no payment API performs well when the eligibility layer feeding it is stale.

Frequently Asked Questions

Frequently Asked Questions

How do you accept FSA/HSA payments?

Accepting HSA/FSA payments requires three aligned elements: an approved healthcare MCC, IIAS configuration for item-level eligibility validation, and a processor that supports HSA/FSA card authorization (natively, like Flex or NMI, or with configuration, like Stripe). If any one of these is missing, legitimate transactions will be declined.

What technology can you buy with FSA?

FSA funds cover health-related technology — blood pressure monitors, glucose meters, CPAP machines, and some digital health subscriptions — but not general consumer electronics. Eligibility follows IRS Section 213(d) and individual plan rules; some items require a Letter of Medical Necessity.

What is IIAS and why does it matter for HSA/FSA payment APIs?

IIAS (Inventory Information Approval System) is a SIGIS-governed standard that allows merchants without healthcare MCCs to validate item-level eligibility at checkout. It enables HSA/FSA cards to be approved at mixed retailers by flagging which items qualify. Without IIAS support, many valid transactions at health retailers are declined at the network level.

What is the difference between HSA and FSA from a payment processing standpoint?

Both use pre-tax funds for qualified medical expenses via a payment card. HSAs allow mid-year contribution changes and fund rollover, so authorization logic must handle dynamic spending limits. FSAs have fixed annual limits that reset yearly, and unused funds are typically forfeited, making payroll-level contribution accuracy especially important.

Do I need a specific merchant category code to accept HSA/FSA payments?

Yes. HSA/FSA card networks restrict card usage to approved healthcare MCCs, and transactions routed through the wrong MCC will be declined regardless of whether the item is medically eligible. Merchants outside standard healthcare MCCs can achieve compliance through IIAS certification or, if they qualify, the 90% Rule.

Can HSA/FSA cards be used for telehealth or digital health subscriptions?

Many telehealth services and digital health subscriptions qualify following CARES Act guidance, but the payment API must support recurring HSA/FSA card billing and the platform must confirm the service qualifies under the member's plan. Flex is specifically built for this use case in subscription-based health apps.