This guide is written for HR teams, benefits administrators, benefits technology platforms, and TPAs. It covers who must comply, which events trigger COBRA obligations, every required notice and its deadline, the full penalty structure, and the mistakes that most commonly land employers in legal trouble.

TL;DR

- Federal COBRA covers private-sector employers and most state/local governments with 20+ employees; state mini-COBRA laws may extend obligations to smaller employers.

- Seven qualifying events trigger COBRA rights, with coverage lasting 18 or 36 months depending on the event.

- Missing a notice deadline triggers IRS excise taxes of $100/day per beneficiary plus simultaneous DOL civil penalties up to $110/day.

- Beneficiaries have 60 days to elect COBRA and 45 days to make the first premium payment after electing.

- Legal responsibility for COBRA compliance stays with the employer even when a TPA handles administration.

What Is COBRA Compliance and Who Must Follow It?

COBRA — the Consolidated Omnibus Budget Reconciliation Act of 1985 — requires covered group health plans to offer continuation coverage to qualified beneficiaries when their coverage would otherwise end due to a qualifying event. Qualified beneficiaries include the covered employee, their spouse, and dependent children.

Employer Coverage Threshold

- Private-sector employers that maintained 20 or more employees on more than 50% of typical business days in the prior calendar year

- Most state and local governments, regardless of size

- Both full-time and part-time employees count toward the 20-employee threshold

Exempt from federal COBRA: Federal government plans and most church plans.

If you fall below the 20-employee threshold, check your state. Many states have "mini-COBRA" laws extending similar obligations to smaller employers — and four states have enacted post-COBRA laws that extend coverage beyond federal timeframes.

What Plans Are Covered

Once you've confirmed your employer obligation, the next question is which plans are in scope. COBRA covers group health plans providing:

- Medical, surgical, and hospital care

- Prescription drugs

- Dental and vision coverage

- Health Flexible Spending Accounts (FSAs)

COBRA does not extend to plans offering only life insurance or disability benefits.

The 7 COBRA Qualifying Events

A qualifying event is any occurrence that causes a covered individual to lose group health coverage. The type of event determines who qualifies as a beneficiary and how long coverage must run.

18-Month Events (Employee + Dependents)

- Termination of employment — voluntary or involuntary, for any reason except gross misconduct

- Reduction in hours — moving from full-time to part-time status, causing loss of coverage

36-Month Events (Spouse and Dependents)

- Death of the covered employee

- Divorce or legal separation

- Employee becoming entitled to Medicare

- Dependent child losing dependent status — aging out at 26 under ACA rules

- Employer bankruptcy (Chapter 11) — covers retired employees and their dependents

Two Important Extensions

Disability extension — extends 18-month coverage to 29 months:

- Trigger: SSA disability determination received during the first 60 days of COBRA

- Notification deadline: 60 days from the SSA decision

- Premium impact: plan may charge up to 150% (vs. the standard 102%) during months 19–29

Second qualifying event extension — extends 18-month coverage to 36 months from the original qualifying event date:

- Trigger: a second event (death, divorce, Medicare entitlement) occurs while a dependent is already on 18-month COBRA

- Notification deadline: 60 days from the second qualifying event

- Common failure point: missing the 60-day window eliminates the extension entirely

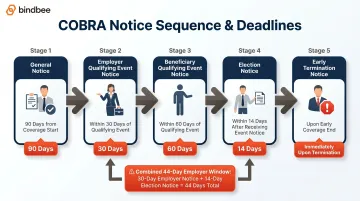

COBRA Notice Requirements: Types, Timelines, and Deadlines

COBRA compliance is essentially a notice-and-deadline system. There are five required notices, each with a distinct sender, recipient, and deadline. A failure at any step creates liability.

Notice Deadlines at a Glance

| Notice | Responsible Party | Deadline |

|---|---|---|

| General Notice (Initial Rights) | Plan administrator | Within 90 days of coverage start |

| Employer Notice of Qualifying Event | Employer | 30 days after employer-triggered event |

| Beneficiary Notice of Qualifying Event | Employee/beneficiary | 60 days after beneficiary-triggered event |

| Election Notice | Plan administrator | 14 days after receiving qualifying event notice |

| Combined window (if employer = plan admin) | Employer/plan admin | 44 days total from qualifying event |

General Notice

The plan administrator must provide a General COBRA Notice to all newly enrolled employees and their covered spouses within 90 days of coverage starting. It must explain COBRA rights, continuation procedures, and key contact information. The DOL provides a model General Notice that serves as a safe harbor against deficiency claims.

Employer Notice of Qualifying Event

For employer-triggered events — termination, reduction in hours, death, Medicare entitlement, or employer bankruptcy — the employer must notify the plan administrator within 30 days.

For beneficiary-triggered events — divorce, legal separation, or a dependent losing status — the employee or beneficiary carries the notification responsibility and has 60 days to notify the plan administrator.

Election Notice and Election Period

After receiving notice of a qualifying event, the plan administrator has 14 days to send a COBRA Election Notice to all qualified beneficiaries. If the employer and plan administrator are the same entity, the total window from the qualifying event is 44 days.

The Election Notice must include the qualifying event, available coverage options, monthly premium amounts, and the election deadline. Beneficiaries then have 60 days from the later of their coverage loss date or the date they received the notice to elect or waive COBRA.

Meeting these deadlines consistently depends on knowing when a qualifying event occurred — the moment it happens, not days later. Benefits administration platforms using Bindbee's unified API receive webhook notifications as soon as a qualifying event is recorded in the source HRIS: terminations, hours reductions, dependent changes, divorce, or dependent age-out. ThrivePass used this approach to automate termination offboarding across COBRA admins, FSA custodians, and payroll systems — cutting manual coordination from days to minutes and eliminating missed deadlines entirely.

Premium Payment Rules

- First payment: Beneficiaries have 45 days from election to pay — this can cover multiple back months retroactively.

- Ongoing payments: Plans must allow a minimum 30-day grace period for each monthly premium.

- Maximum premium: 102% of full plan cost during standard coverage; 150% during the disability extension (months 19–29).

Early Termination Notice

If COBRA ends before the maximum period — most often due to non-payment after the grace period — the plan administrator must send an Early Termination Notice informing the beneficiary of the end date and reason. This notice is mandatory even when coverage ends for non-payment. Skipping it is itself a compliance violation.

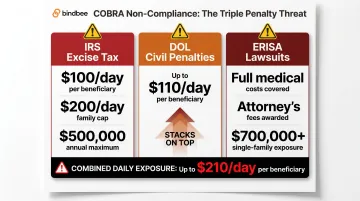

Penalties for COBRA Non-Compliance

The penalty structure for COBRA failures is layered, and each layer runs simultaneously with the others.

IRS Excise Tax (IRC Section 4980B)

- $100 per day per qualified beneficiary for each day of noncompliance

- $200 per day cap when multiple family members in the same household are affected

- Annual cap for unintentional failures: The lesser of $500,000 or 10% of prior-year group health plan costs

- If the failure is discovered during an IRS examination, the minimum tax jumps to $2,500 (or $15,000 if the failure is more than de minimis)

DOL Civil Penalties (ERISA 502(c)(1))

The DOL can separately assess up to $110 per day per qualified beneficiary for failure to provide required election notices. These penalties stack on top of IRS excise taxes — a single missed Election Notice can generate combined exposure of up to $210/day per beneficiary.

ERISA Private Right of Action

Qualified beneficiaries can sue directly under ERISA to recover:

- The full cost of medical expenses incurred while they should have had COBRA coverage

- Statutory penalties

- Attorney's fees

Litigation exposure can dwarf the regulatory penalties. In Marrow v. E.R. Carpenter Co. (M.D. Fla., February 2025), potential liability exceeded $700,000 for a single family — before accounting for medical expenses and other class members. Wells Fargo and Auto Club Group each settled COBRA notice class actions for $1 million.

The TPA Liability Trap

Delegating COBRA administration to a TPA does not transfer legal responsibility. In Howard v. Ivy Creek of Tallapoosa, LLC (2022), the court held the employer liable for a missed notice even though the TPA was contractually obligated to send it. The employer had even sent a separate dental notice to the correct address — proving they had current contact information.

Employers must be prepared to demonstrate good-faith compliance efforts independent of what the TPA contract says. The obligation stays with the plan sponsor.

Common COBRA Compliance Mistakes Employers Make

EBSA closed 729 civil investigations in FY 2024, with 71% producing monetary results or corrective action and $741.9 million recovered through enforcement alone. More than a decade of court decisions — catalogued by Jackson Lewis as a "mushrooming" litigation trend — confirm that administrative shortcuts carry real financial consequences.

Delayed Qualifying Event Reporting

Managers often fail to report terminations, hour reductions, or divorces to HR promptly. This compresses the available notice window and makes the 44-day deadline nearly impossible to hit. Reduction in hours is the most commonly overlooked trigger — many HR teams know to process terminations but miss the hours-reduction category entirely.

Incomplete Beneficiary Identification

Employers often process COBRA only for the departing employee and miss their covered dependents — who are each independent qualified beneficiaries with their own election rights. This gap is most acute in divorce situations, where the former spouse never receives a legally required Election Notice.

Missing Documentation

Sending a notice means nothing without proof of delivery. Employers who can't produce certified mail receipts or delivery logs have no defense if a beneficiary claims non-receipt.

Documentation failures are the most common reason employers lose ERISA lawsuits related to COBRA. The most cited failure modes:

- No certified mail receipt or delivery confirmation

- Notice sent to a stale or incorrect address (see Howard v. Ivy Creek)

- No delivery log to rebut a beneficiary's non-receipt claim

Frequently Asked Questions

What is COBRA compliance?

COBRA compliance is an employer's legal obligation under the Consolidated Omnibus Budget Reconciliation Act to offer qualified beneficiaries the option to continue group health coverage after a qualifying event, along with issuing all required notices within specified deadlines. The IRS and DOL each enforce their own set of requirements — and both can penalize non-compliant employers independently.

What are the 7 COBRA qualifying events?

The seven qualifying events are:

- Termination of employment (except for gross misconduct)

- Reduction in hours

- Death of the covered employee

- Divorce or legal separation

- Employee enrollment in Medicare

- Loss of dependent status (such as aging out at 26)

- Employer bankruptcy

The first two trigger 18 months of coverage; the remaining five trigger 36 months.

What is the employer size threshold for COBRA compliance?

Federal COBRA applies to private-sector employers and most state/local governments with 20 or more employees on more than 50% of typical business days in the prior calendar year. Employers below this threshold may still face obligations under their state's mini-COBRA law.

How long does an employer have to give COBRA information?

The employer has 30 days to notify the plan administrator of a qualifying event. The plan administrator then has 14 days to send the Election Notice. When both roles belong to the same entity, the combined window is 44 days.

What is the 60-day rule for COBRA?

There are two separate 60-day rules. First, qualified beneficiaries have 60 days from the later of their coverage loss date or the Election Notice date to elect COBRA. Second, employees and beneficiaries have 60 days to notify the plan administrator of beneficiary-triggered qualifying events like divorce or loss of dependent status.

What are the penalties for non-compliance with COBRA?

Penalties come from three separate sources:

- IRS excise taxes: $100/day per beneficiary, capped at $200/day per family (annual max: $500,000 or 10% of group health plan costs for unintentional failures)

- DOL civil penalties: Up to $110/day per beneficiary, stacked on top of IRS exposure

- ERISA lawsuits: Full medical costs plus attorney's fees — single-family exposures have exceeded $700,000