The IRS actively enforces the employer mandate. Penalty amounts increase annually, and Letter 226J notices continue to go out to employers who fall short on coverage offers, affordability, or reporting accuracy. What makes this particularly frustrating is that most penalties aren't intentional — they're the product of fragmented systems, manual processes, and workforce complexity that catches HR and benefits teams off guard.

Understanding what triggers IRS enforcement is the first step toward staying protected.

TL;DR

- ALEs (50+ full-time equivalent employees) must offer affordable, minimum-value coverage and file accurate 1094-C/1095-C forms annually

- Two penalty categories apply: Section 4980H (coverage failures) and IRC 6721/6722 (reporting errors) — and employers can be hit with both

- Most penalties trace back to misclassified employee status, affordability miscalculations, or data gaps between HR, payroll, and benefits systems

- Prevention requires year-round tracking and integrated data — not an end-of-year scramble

- IRS Letter 226J triggers a 90-day response window — documented proof of compliance can reduce or eliminate the penalty

Understanding ACA Employer Obligations

Who Qualifies as an ALE?

An employer is an Applicable Large Employer if it averaged 50 or more full-time employees — including full-time equivalents (FTEs) — during the prior calendar year. One important detail that catches employers off guard: "full-time" under the ACA means 30+ hours per week or 130 hours per month, not the traditional 40-hour standard.

Companies with common ownership are counted together under IRC Section 414 controlled group rules. A subsidiary with 30 employees isn't off the hook if the parent company pushes the combined total past 50.

The Three Core Obligations

Qualifying as an ALE triggers three distinct obligations:

- Offer minimum essential coverage that meets minimum value to at least 95% of full-time employees and their dependents

- Furnish Form 1095-C to each full-time employee by the annual deadline (March 2, 2026 for the 2025 tax year)

- File Forms 1094-C and 1095-C with the IRS electronically by March 31, 2026 for the 2025 tax year — required for employers filing 10 or more information returns

Each obligation carries its own penalty exposure. An employer can owe coverage penalties under 4980H(a) or 4980H(b) and face separate reporting fines — all from the same tax year.

Common Causes of ACA Compliance Penalties

Most ACA penalties come from process gaps rather than deliberate non-compliance. Here are the most common triggers:

Misclassifying Employee Work Status

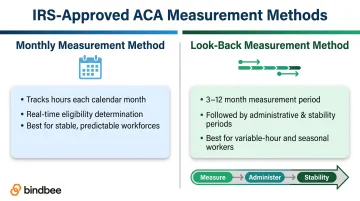

Incorrectly categorizing full-time employees as part-time — or failing to count variable-hour workers using IRS-approved measurement methods — is a primary driver of Section 4980H penalties. Seasonal workforces, high-turnover roles, and employees whose hours fluctuate are especially prone to misclassification.

The IRS provides two approved methods: the monthly measurement method (tracking hours each calendar month) and the look-back measurement method (using a defined 3–12 month measurement period to determine status before a stability period). Employers using informal or inconsistent approaches expose themselves to retroactive liability.

Missing or Late Coverage Offers

Coverage must be offered within specific timeframes tied to measurement and stability periods. Waiting until open enrollment, or until an employee files a complaint, is too late. A single employee receiving a Premium Tax Credit (PTC) through the Marketplace can trigger the 4980H(a) "sledgehammer" penalty across the entire workforce.

Affordability Miscalculations

Coverage is only ACA-compliant if the employee's share of the lowest-cost self-only plan doesn't exceed the affordability threshold: 9.02% of household income for 2025, rising to 9.96% for 2026. Employers using the wrong safe harbor method or applying outdated rate assumptions may unknowingly offer plans that trigger 4980H(b) penalties.

Inaccurate or Untimely IRS Reporting

Errors on Form 1095-C — wrong offer codes on Line 14, incorrect safe harbor codes on Line 16, missing Social Security numbers, or incorrect coverage dates — generate penalties under IRC 6721/6722 entirely separate from whether compliant coverage was offered. An employer can offer perfect coverage and still face reporting penalties for sloppy paperwork.

Warning Signs You're Approaching an ACA Compliance Problem

Watch for these early indicators:

- HR and payroll data don't reconcile consistently across systems

- Coverage offers are tracked in spreadsheets or manually managed

- Benefits enrollment deadlines are handled reactively, without automated eligibility workflows

- Variable-hour employees have no formal measurement period process in place

Types of ACA Penalties Employers Face

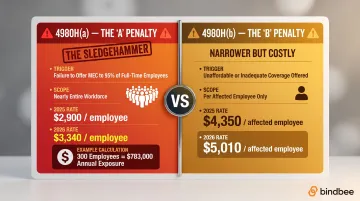

Section 4980H(a) — Failure to Offer Coverage

The "A penalty" is the most dangerous. When an ALE fails to offer minimum essential coverage to at least 95% of full-time employees and even one employee receives a Premium Tax Credit through the Marketplace, the penalty applies to nearly the entire workforce.

Per IRS Rev. Proc. 2025-26, the 2025 rate is $2,900 per full-time employee annually (minus a 30-employee reduction). For a 300-employee company, that's 270 × $2,900 = $783,000 in annual exposure from a single coverage gap. The rate rises to $3,340 per employee for 2026.

Section 4980H(b) — Unaffordable or Inadequate Coverage

The "B penalty" is narrower but still costly — it applies per employee who actually receives a PTC because the offered coverage was unaffordable or didn't meet minimum value (covering at least 60% of total allowed costs). The 2025 rate is $4,350 per affected employee, rising to $5,010 in 2026.

Failure to File or Furnish Forms 1094-C / 1095-C

Reporting penalties under IRC 6721/6722 are assessed separately and stack — one penalty for failing to file with the IRS, another for failing to furnish to employees:

| Filing Timing | Penalty Per Return |

|---|---|

| Within 30 days of due date | $60 |

| 31 days to August 1 | $130 |

| After August 1 | $330 |

| Intentional disregard | $660 (no cap) |

A 500-employee company that completely fails to file faces up to $330,000 in reporting penalties alone — before any 4980H exposure.

IRS Letter 226J

Letter 226J is the IRS's formal notice proposing an Employer Shared Responsibility Payment. It includes three components:

- Penalty summary — proposed amount broken down by month

- Form 14764 — the official response form

- Form 14765 — lists each employee who received a PTC

The Employer Reporting Improvement Act, signed December 23, 2024, extended the response window from 30 to 90 days for returns due after December 31, 2024. Use that window to review Form 14765 line by line, gather supporting documentation, and prepare a rebuttal if the proposed amount is incorrect.

Employers who don't respond by the deadline face an automatic Notice and Demand for the full proposed amount.

How to Avoid ACA Compliance Penalties

Prevention requires year-round processes, not last-minute corrections.

Track Employee Hours and Status Continuously

Implement a formal IRS-approved measurement method — particularly for variable-hour and seasonal workers. The look-back measurement method provides predictability: measure hours over a defined period (typically 3–12 months), then apply a coverage determination for the subsequent stability period. This must run continuously, not just at open enrollment.

Apply ACA Affordability Safe Harbors Correctly

The IRS offers three safe harbors for demonstrating coverage affordability:

| Safe Harbor | Best For |

|---|---|

| W-2 Wages | Consistent salaried employees; applied after year-end |

| Rate of Pay | Hourly workers; calculated prospectively (hourly rate × 130 hours) |

| Federal Poverty Line | Uniform application across all employees regardless of wages |

Document which safe harbor you use for each employee class and apply it consistently. Switching methods mid-year or applying the wrong method to a workforce segment can create affordability failures.

Automate ACA Reporting Workflows and Deadlines

Manual spreadsheet-based processes break under workforce complexity. Benefits administration platforms need dedicated ACA reporting capabilities that:

- Generate accurate 1095-C line codes automatically

- Flag data errors before submission

- Track IRS filing deadlines with automated alerts

The Paperwork Burden Reduction Act (also signed December 23, 2024) now allows electronic furnishing of Form 1095-C — employers can post forms on a secure website and notify employees, eliminating mandatory paper mailings. This is a meaningful cost reduction for large employers.

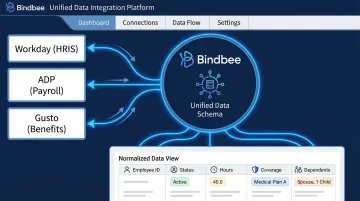

Integrate Data Across HRIS, Payroll, and Benefits Systems

This is where most compliance programs break down. ACA compliance requires synthesizing employment status from HRIS, hours data from timekeeping systems, and coverage elections from benefits platforms — and those systems rarely communicate natively.

When data is siloed, specific gaps emerge:

- An employee's status changes in the HRIS but doesn't update in the benefits platform for weeks, causing a missed eligibility window

- Hours from timekeeping don't reconcile with payroll records, making measurement period calculations unreliable

Benefits administration platforms that connect to a unified data layer avoid this entirely. Bindbee's API normalizes employment status, hours worked, coverage elections, dependent data, and effective dates across 60+ HRIS and payroll systems — including Workday, ADP, Gusto, Rippling, and Paychex — into a single consistent schema. Platforms using this infrastructure get real-time eligibility signals, dependent enrollment data with relationship types and SSNs, and payroll deductions mapped correctly across different pay cycles. That eliminates the source of most ACA data errors before they reach filing time.

Conduct Pre-Filing Data Audits

Before submitting 1094-C/1095-C forms, run reconciliation checks:

- Verify SSNs match IRS records

- Confirm every employee coded as offered coverage received a timely offer

- Review affordability calculations against current safe harbor thresholds

- Check that coverage dates on 1095-C forms match actual offer and enrollment records

Catching errors pre-submission costs far less than filing corrected returns or disputing a Letter 226J assessment.

Long-Term Best Practices for Staying ACA-Compliant

ACA compliance is an ongoing operational discipline, not a one-time project. These practices reduce cumulative risk over time:

Assign ownership of ACA tasks across HR, payroll, benefits, and IT with documented deadlines tied to measurement period end dates and IRS filing windows.

Update affordability calculators every plan year — the 4980H(a) penalty is $3,340 in 2026 and already announced at $3,180 for 2027, and thresholds shift annually.

Trigger eligibility reviews automatically on new hires, terminations, and dependent changes. Real-time webhooks (such as Bindbee's life event notifications) let benefits teams act before deadlines pass, not after filing season exposes the gap.

Keep records of every coverage offer, employee acceptance or waiver, affordability calculation, and hours log. If it isn't documented, an IRS auditor will treat it as if it never happened.

Frequently Asked Questions

Are there still ACA penalties?

Yes. The IRS continues to actively enforce the employer mandate and issue Letter 226J notices proposing Employer Shared Responsibility Payments. Penalty amounts are inflation-adjusted annually — both the 4980H(a) and 4980H(b) rates increased for 2025 and will increase again for 2026.

How do you avoid an ACA penalty?

Track full-time employee status year-round using IRS-approved measurement methods, offer affordable minimum-value coverage within required timeframes, integrate HR/payroll/benefits data to eliminate eligibility gaps, and file accurate 1094-C/1095-C forms by IRS deadlines.

Who qualifies as an Applicable Large Employer under the ACA?

An ALE is an employer that averaged 50 or more full-time employees (including FTEs) during the prior calendar year. Controlled groups of related companies are counted together for this threshold, meaning a smaller subsidiary can still be an ALE member if the combined headcount exceeds 50.

What is IRS Letter 226J and what should employers do when they receive one?

Letter 226J is the IRS's proposed Employer Shared Responsibility Payment notice. Employers have 90 days to respond (for returns due after December 31, 2024) using Form 14764, with documentation to dispute, correct, or accept the assessment. Missing that deadline results in automatic penalty finalization.

What is the difference between the 4980H(a) and 4980H(b) penalties?

The "A" penalty applies when an employer fails to offer minimum essential coverage to at least 95% of full-time employees and at least one employee receives a Marketplace tax credit, exposing nearly the entire workforce to the assessment. The "B" penalty is narrower, applying only to each specific employee who receives a tax credit because the offered coverage was unaffordable or didn't meet minimum value.

What data do employers need to maintain for ACA compliance?

Employers need to maintain and reconcile four core data categories across HR, payroll, and benefits systems year-round:

- Employee hours worked and employment status changes

- Records of coverage offers with employee acceptance or waiver

- Dependent enrollment data with effective dates

- Affordability calculations tied to the applicable safe harbor