This guide covers what waiting periods are, how the ACA governs them, the structures employers actually use, and what drives those decisions — whether you're designing a benefits program, building a benefits platform, or just trying to make sure new hires don't fall through the cracks.

TL;DR

- The ACA caps waiting periods at 90 consecutive calendar days — weekends and holidays count

- Employers can offer coverage starting on day one, and many do to attract talent

- The enrollment deadline (when elections must be submitted, typically 30 days) is separate from the waiting period (when coverage activates)

- "1st of the month after 90 days" is not ACA-compliant: it can push eligibility past the 90-day ceiling

- Probationary periods don't restart the clock — the waiting period begins on day one of employment

What Is a New Hire Waiting Period for Health Insurance?

A waiting period is the time between an employee's first day of employment and the date they become eligible to enroll in or activate employer-sponsored health coverage. The employer sets it, within limits defined by federal law.

Three terms regularly get conflated:

- Waiting period — determines when coverage activates. Set by the employer, capped by the ACA at 90 calendar days.

- Enrollment deadline — the window during which a new hire must submit their plan elections, typically 30 days from hire — a plan-document convention, not a federally fixed requirement.

- Probationary period — a performance evaluation window. It may run concurrently with the waiting period, but it does not extend or replace it.

The practical implication: a new hire can submit their benefit elections on day three of employment while still in a 60-day waiting period. Their elections are on file; coverage activates when the waiting period ends.

The ACA's 90-Day Rule: What Employers Must Know

Under the Affordable Care Act (effective for plan years beginning on or after January 1, 2015), group health plans cannot impose a waiting period exceeding 90 consecutive calendar days. This applies to all employers that offer group health coverage, regardless of size, including grandfathered plans.

The Calendar Day Requirement

"90 calendar days" means exactly that. Weekends, federal holidays, and days the office is closed all count. Coverage must be available no later than day 91. If day 91 falls on a Saturday, coverage must be active on or before that day — not the following Monday.

The "1st of Month After 90 Days" Trap

This is the most common compliance error still in the wild. Consider an employee who starts on May 23. Ninety calendar days from May 23 is August 21. But "1st of the month after 90 days" pushes the coverage start date to September 1 — that's 101 days after hire. That structure is non-compliant under the ACA.

The DOL's ACA FAQs Part XVI explicitly flagged this configuration. Any plan design still using month-based phrasing tied to "after 90 days" needs an immediate audit.

Probationary Periods and the Clock

The ACA permits a legitimate orientation period ("bona fide" in ACA terms) of up to one calendar month before the 90-day clock starts. Two rules govern what happens next:

- Once orientation ends, the 90-day countdown begins and cannot be paused or reset by a performance review

- Stacking is non-compliant — a 90-day probationary period followed by a separate 90-day waiting period pushes eligibility well past the federal limit

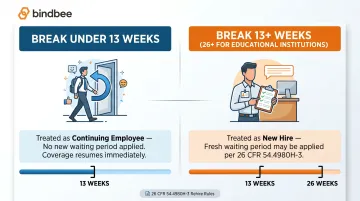

Rehire Rules

Break-in-service thresholds under 26 CFR 54.4980H-3 determine whether a rehire gets a fresh waiting period:

- Break of 13+ weeks (26+ weeks for educational institutions): the employee may be treated as a new hire and a new waiting period applied

- Break under 13 weeks: the employee is treated as a continuing employee — coverage resumes without a fresh waiting period

Benefits platforms that track these thresholds automatically avoid the compliance gaps that surface when rehire logic is handled manually or inconsistently across systems.

Non-Compliance Consequences

Waiting periods that exceed the 90-day limit can trigger the group market-reform excise tax under IRC 4980D — $100 per day per affected individual. For a benefits platform or employer managing hundreds of new hires, that exposure adds up fast.

Common Waiting Period Structures Employers Use

Most employers cluster between day-one and 60 days. According to the 2025 KFF Employer Health Benefits Survey, 32% of covered workers face no waiting period at all, and another 26% wait one month or less. Only 18% face a three-month wait — and any three-month structure needs careful calendar-day verification.

Here are the four common compliant structures:

| Structure | How It Works | Notes |

|---|---|---|

| Immediate / Day One | Coverage begins on the hire date | No waiting period; strongest recruiting signal |

| 1st of month following hire | Coverage starts the first of the next calendar month | If hired June 1, coverage starts July 1 |

| 1st of month following 30 days | Short buffer before aligning to a billing cycle | Balances admin simplicity with brief delay |

| 1st of month following 60 days | Moderate delay, aligns with many probationary timelines | Check that no hire date pushes this past day 90 |

"1st of month following 90 days" is not on this list — it's no longer permissible. For employees hired mid-month, that structure routinely exceeds 90 calendar days.

The Enrollment Deadline Layer

Whatever structure an employer chooses, the enrollment deadline runs separately. New hires typically have 30 days from their hire date to submit plan elections.

Missing that window generally means waiting until the next annual open enrollment or a qualifying life event — a gap that can leave employees uninsured for months. Both deadlines should be communicated at the start of onboarding, not buried in a welcome packet.

What New Hires Can Do During the Waiting Period

Employees have several concrete options for maintaining coverage during the gap:

- Marketplace Special Enrollment Period — losing job-based coverage (including at a previous employer) triggers an SEP. Employees have 60 days to apply, with coverage starting the first of the month after the loss date. Premium tax credits may be available based on income.

- Spouse or domestic partner's employer plan — HIPAA special enrollment rules give employees 30 days to enroll in a spouse's group plan following loss of other coverage, marriage, birth, or adoption.

- COBRA from a previous employer — keeps prior coverage active but at the full premium plus an administrative fee. Expensive, but useful for short gaps or employees with ongoing care needs.

- Short-term health plans — largely eliminated as a practical option. A 2024 HHS/DOL/Treasury rule limits these to no more than 3 months per contract and 4 months total for policies beginning on or after September 1, 2024.

Key Factors That Influence Waiting Period Decisions

Talent Competition

Health benefits are a material factor in hiring decisions. SHRM's 2025 Employee Benefits Survey found that 88% of employers rate health-related benefits as extremely or very important to their workforce strategy. For candidates comparing multiple offers, a day-one coverage policy is a concrete differentiator — especially in industries where skilled workers have real choices.

Cost and Administrative Factors

Longer waiting periods serve specific operational purposes:

- Reduced benefit costs from employees who leave before completing their first few months

- Simpler billing when coverage start dates align with the first of a payroll month

- Carrier-specific participation thresholds for small-group enrollment (set by carriers and states, not the ACA)

Neither reason justifies exceeding 90 days, but they explain why many employers don't rush to offer immediate coverage.

Multi-Class Employer Groups

Larger employers can set different waiting periods for different employee classes — full-time vs. part-time, salaried vs. hourly, managers vs. line staff — as long as the classification is non-discriminatory and applied consistently. This is where benefits administration infrastructure becomes operationally critical.

When different employee groups have different eligibility dates, manual tracking of who becomes eligible when is error-prone at scale. Benefits platforms need accurate, real-time hire date and benefit class data to trigger enrollment windows correctly — and most can't afford to rebuild that logic from scratch for every employer they onboard.

Bindbee's eligibility intelligence layer handles waiting period calculation across plan configurations and benefit class assignment based on employment type, location, salary tier, and tenure, so connected benefits platforms get that logic out of the box.

When a new hire record appears in a connected HRIS system, Bindbee fires a webhook instantly — pushing normalized employee, dependent, and eligibility data to connected benefits platforms without manual intervention. ThrivePass cut new hire onboarding from six weeks to under one week using this approach, with coverage activating on day one instead of day 30.

Common Misconceptions About New Hire Waiting Periods

"90 days equals 3 months"

It doesn't, and this distinction causes compliance failures. Calendar months vary in length, so a policy written as "three months" can mean 89, 91, or 92 days depending on when the hire date falls. The ACA rule is strictly 90 consecutive calendar days — not three months. Plan documents and system configurations should express waiting periods in days, not months. A benefits platform that calculates eligibility from hire date in months will produce incorrect effective dates for employees hired in January, March, or any other month with more or fewer than 30 days.

"The probationary period and waiting period are separate clocks"

Many HR teams still operate as though a 90-day performance trial runs first, and then a health insurance waiting period begins afterward. That's non-compliant. The waiting period starts on day one of employment (or after a legitimate orientation period of no more than one calendar month). Structuring a plan document to say coverage begins "after the probationary period" effectively extends the waiting period beyond 90 days — a direct ACA violation with potential excise tax exposure.

"All employees have to wait"

The 90-day rule is a ceiling, not a floor. Employers can offer coverage starting on the first day of employment, and many do — particularly in competitive hiring markets or industries where benefits are a primary attraction lever. Whether to use that ceiling at all is a business decision, not a legal requirement.

Frequently Asked Questions

How long do you have to wait for health insurance when starting a new job?

It depends on your employer. The ACA caps waiting periods at 90 consecutive calendar days, but many employers use shorter windows — 30 or 60 days are common — and some offer coverage starting on day one. Check your offer letter or benefits guide for the specific structure.

What is the 90-day rule for health insurance?

The ACA's 90-day rule requires employers who offer group health coverage to make otherwise-eligible employees eligible for coverage within 90 consecutive calendar days of their hire date. Pushing eligibility past day 91 is a federal compliance violation subject to excise tax penalties.

Why do employers make new hires wait 90 days for health insurance?

Waiting periods help employers manage benefit costs, reduce administrative burden from early-tenure turnover, and align coverage start dates with payroll or billing cycles. The full 90 days is the maximum permitted, not a required duration — many employers use shorter windows or no wait at all.

Do ACA rules allow employers to impose a waiting period?

Yes. The ACA explicitly permits waiting periods of up to 90 days. What it prohibits is any plan structure that delays an eligible employee's coverage past the 91st calendar day of employment.

How long after starting a job do you have to enroll in benefits?

The enrollment window is typically 30 days from your hire date, set by the employer's plan document rather than federal law — separate from the waiting period itself. Missing the enrollment deadline usually means waiting until the next annual open enrollment or a qualifying life event.

Is there health insurance with no waiting period for new hires?

Yes. Employers can offer day-one coverage with no waiting period, and many do as a recruiting and retention strategy. If immediate coverage is a priority, ask during the hiring process — the answer varies widely by employer and industry.